You have just made a big decision—to pursue your education. Whether you want to go to a vocational school, college or university, you need to choose how you will pay for the costs associated with your education, like tuition and school fees, school supplies, transportation and housing. Now, you need to decide which of the options available to you best fit your needs.

It is important to understand the characteristics and implications of each financing option to help you make the best decision based on your financial needs and resources.

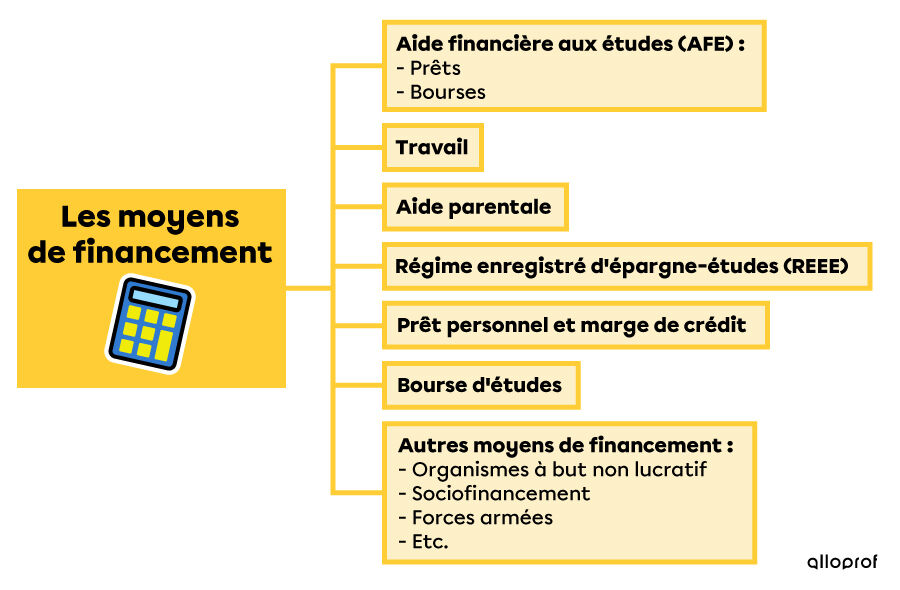

Your first step is to apply for Student Financial Assistance. This loan and bursary program is managed by the Quebec government. These loans and bursaries can provide financial support to students who do not have enough money to start a secondary-level vocational training or post-secondary academic program.

Find out more about the eligibility criteria for this program on the Student Financial Assistance website.

You can check whether you are eligible for the government’s loan and bursary program by completing a financial assistance simulation before submitting a real application. This will give you an idea of the amount of money you may be entitled to receive.

As this is a simulated calculation, the amounts suggested by the student financial assistance calculator may differ from what you might actually get.

Nicolas is single and does not receive any financial help from his parents, because their salaries are not high enough. He lives with his father all year while attending college: his program runs from September to August. This year, Nicolas worked as a gas station attendant until school began, and then he decided to focus entirely on his nursing program. When he looks at his tax return, he realizes that his total income is $7,000 and his tuition fees for the semester are $200. After entering this information into the student financial assistance calculator, he finds out that he could receive $912 in loans and $430 in bursaries.

Sandra is a student who has been married to Jean-François for three years. They do not have children. During the year, Sandra worked as a part-time waitress in a local restaurant. Recently, she decided to enroll in a business management program with the goal of owning her own bistro one day. She saved up $12,000 for the upcoming semester, which will cost her $160. Her husband earned $30,000 the previous year. After entering this information into the student financial assistance calculator, she learned that she could receive $912 in loans and $2,533 in bursaries.

As you can see from these examples, the student financial assistance program considers many things when determining the amount given or loaned to you. For example, the government believes that John can help pay for Sandra’s education because they are married. This is called a contribution. Contributions are included in the calculation of the amount of money granted by the government, as well as eligible expenses, meaning all costs related to education.

Contributions are the amounts of money that students and their families can provide to help pay for school.

The student financial assistance program relies on the gross incomes of parents and students to establish what amount of money may be offered. For example, if both parents earn less than $45,000 a year, the student financial assistance program considers that they cannot contribute to their child’s education. Find more information on this topic at the following link: Parents’ contribution.

Here is how the government calculates the amount it provides:

Eligible Expenses - Contributions = Financial Needs

Financial needs are the amount you will receive in loans and bursaries.

Eligible expenses are the total of monthly expenses or living expenses, such as housing, food and transportation, and one-time expenses like tuition fees and school supplies.

You just found out that you can get a $960 loan and a $645 bursary for the coming year, but you’re having trouble understanding the difference between a loan and a bursary. Do these amounts of money belong to you? Do you have to pay any of it back to the government?

The good news is you do not have to give the bursary back to the government. Unfortunately, you do have to pay back the student loan, but not until you have finished your studies, so you have a break while you are still in school.

Find out more about your student loan repayment options on the student financial assistance website: Repayment of a Student Debt

You might be hesitant to apply for a student loan through the student financial assistance program, because you think you might be able to get a bigger personal loan than the one offered by the government. Whether you are considering one option or applying for both a student loan and a personal loan, here are some things to consider.

The two loans work in a very similar way, since they are managed by a financial institution, namely a bank or a credit union.

The big difference between a student loan and a personal loan is how interest is repaid. The student loan is a government loan that is for the duration of your studies. This means that you do not have to worry about paying the interest on your loan while you are attending school. With a personal loan, you have to make payments on your loan even while you are a student.

- Interest is an additional amount of money that has to be paid when repaying a loan. This additional amount is based on the interest rate.

-

The interest rate refers to the amount a person or institution has to pay to access a loan. This amount is calculated as a percentage.

The other thing to consider is the interest rate, which is lower for student loans. The total debt is the amount borrowed plus the accumulated interest, which is lower for a student loan than a personal loan.

Getting a job can help pay for your education. Like Nicolas and Sandra, you could choose to work during the summer and use the money earned to reduce your expenses during the school year.

You could also take on a part-time student job and develop skills and increase your confidence. The important thing is to keep a balance between school and work and give yourself the best chance of succeeding in your education.

To find out more about how to achieve a better balance between school and work, see the following concept sheet: Balancing School and Work

Interesting fact: Some academic programs offer paid internships, which are a great way to put into practice what you learn in the classroom. Find out more from your educational institution.

Some parents can provide valuable financial assistance while others do not have the financial resources to support their children’s professional future. This is the case for Nicolas, who applied for Student Financial Assistance to help pay for his nursing program. Your parents might have signed up for a Registered Education Savings Plan (RESP) when you were born. This savings plan gives your parents the means to save money for your future education.

Find out more about how RESPs work on the Canada Revenue Agency’s website: Registered Education Savings Plan (RESP)

One way to pay for your education is with a personal loan or line of credit. Both of these options involve interest on the amount of money borrowed that accumulates from the first day the loan is taken, unlike a student loan.

A personal loan is a fixed amount of money that the bank or credit union gives you in full and then you have to pay back in regular installments until you have paid it off completely. Be aware that you cannot get any additional money once the loan is in your account.

Imagine that, in addition to his student loan, Nicolas has decided to apply for a personal loan from his bank in order to buy a car because his college is more than two hours away from home. His bank loans him $15,000 with an interest rate of 9%, payable at $241.34 per month starting in September, the first month of the loan. This means that he will finish paying back the loan in seven years, without being able to borrow more.

A line of credit works like a credit card, giving you access to a set amount of money from your bank or credit union that you can use in whole or in part, as long as you do not exceed the limit set by your financial institution. For example, if the bank offers you a $5,000 line of credit and you have already spent $4,500, you cannot buy a $600 stove. You will have to pay part of your line of credit back before you can make transactions worth more than $500, because that is the amount of money you have left. Be aware that you have to pay interest, at a favourable rate, throughout your time as a student. When you finish your studies, you will make an agreement with your financial institution to repay the line of credit.

Depending on the academic program you choose, you may be eligible for a scholarship. Do you have an excellent academic record? You should know that some colleges and universities award scholarships for excellence to students who have distinguished themselves with outstanding academic records. You can learn more from your educational institution.

Scholarships can also be awarded for commitment to a specific field of study and to top athletes, and bursaries may also be granted to students with limited financial means or disabilities.

To find out what is available, you should visit the list of scholarships and bursaries of the educational institution where you plan to study.

There are other, lesser-known ways to help you pursue your education. These include:

-

Not-for-profit organisations

-

Foundations

-

Community crowdfunding

-

Armed forces

-

Lifelong Learning Plan (LLP)